The opinions reflected in the following post 'Growth falters, and inequality grows as capital flows' are those of the author. Any errors and omissions are the author's alone.

Former Labor Secretary during the Clinton Administration, Robert Reich, framed it cleverly in an opinion piece for FT.com in dissecting the gaping policy holes of both incumbent and challenger after the Republican and Democratic conventions:

But why should we care about the results of a wounded Global Minotaur? Unlike Theseus leading the Athenians out of the labyrinth, the majority of people have nothing but blind folded politicians to guide them from the maze that is the global economy. We need to re-frame the argument into a long term solution that is sustainable but doing so requires looking at some uncomfortable truths: be it rising inequality, growth of non-productive sectors, or the anemic labour market.

Inequality matters

The case against "excessive" equality

Source: http://visualeconomics.creditloan.com/income-distribution-by-country/

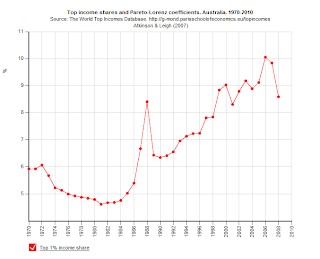

Trends of income shares to the top 1% (1970 - 2009/2010)

The charts below show the income shares (in Australia, Canada, United Kingdom and United States) accruing to the top 1% from the 1970s on and the data was made available by Atkinson, Piketty and Saez of the Paris School of Economics. Go to their website to see these and many more data sets highlighting how inequality is at the highest rate since the 1920s.

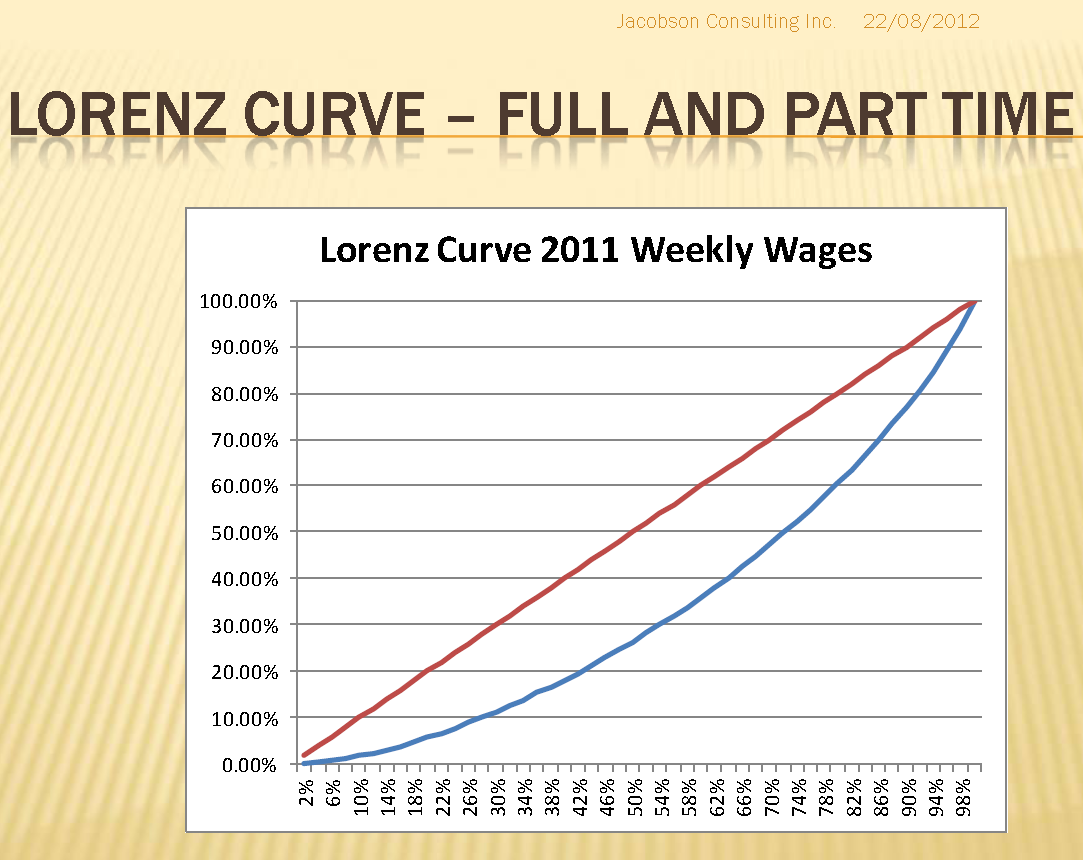

Canadian Wage Distribution Dynamics

The following charts are from a presentation by Paul Jacobson, "Recent Wage Dynamics - Working Paper" that shows inequality in the Canadian context.

Lorenz Curve

Lorenz Curve

Source: Jacobson Consulting

Source: Jacobson Consulting

Social and Economic Mobility

Key Takeaways (please visit Miles Corak's website for more content related to this issue).

Key Takeaways (please visit Miles Corak's website for more content related to this issue).

Source: Miles Corak

Source: Miles Corak

A Broken Economy: What it isn't

A Broken Economy: What it is

Overall model of the FIRE (Finance, Insurance, Real Estate) sector: producers, consumers, government, world (Hudson and Bezemer, 2012: Fig. 4, p.9) based on the U.S. economy primarily but just as relevant to other nations such as the United Kingdom, Spain and Ireland who have suffered real estate asset crashes.

While Arthur Laffer and Stephen Moore continue to use their pulpit at the Wall Street Journal to conclude that the issue of class should be a non issue as "wealth trickles down" in their worldview, the facts on the ground are quite different. The current situation of inequality was built after the embers of the defunct "Golden Age of Capitalism" burnt out conclusively in the 1970s.

(Source: Glyn, Capitalism Unleashed, Ch. 1-2)

(Source: Glyn, Capitalism Unleashed, Ch. 1-2)

(Source: Marglin, Lessons of the Golden Age of Capitalism: p. 25)

(Source: Marglin, Lessons of the Golden Age of Capitalism: p. 25)

What happens when that salaried professional referenced above "whose life prospects are reasonably certain and whose life experience reinforces the notion that he or she is "in control" gives way to a growing cohort of people whose jobs have been outsourced, who work on a contract basis, who lack security and whose career prospects are uncertain at best? We have, in the words of Professor Guy Standing, a group of people living precariously: we have the precariat.

The elite are those few whom the masses cannot relate to but to whom the establishment fawn. Wealth has little reason to trickle down when the super rich do not know what to do with their surplus capital:

The elite are those few whom the masses cannot relate to but to whom the establishment fawn. Wealth has little reason to trickle down when the super rich do not know what to do with their surplus capital:

References:

Bernanke, B. (08, 2012 31). Monetary policy since the onset of the crisis. Retrieved from http://www.federalreserve.gov/newsevents/speech/bernanke20120831a.htm

Hudson, M., and Bezemer, D. (2012). Incorporating the rentier sectors into a financial model. World Economic Review, 1(1), 1-12. Retrieved from http://wer.worldeconomicsassociation.org/article/view/36

Reich, R. (2012, September 07). After the politics, the reality of the us labour market. Financial Times. Retrieved from http://blogs.ft.com/the-a-list/2012/09/07/after-the-politics-the-reality-of-the-us-labour-market/

Graselli, M. R., & Costa Lima, B. (2012). An analysis of the Keen model for credit expansion, asset price bubbles and financial fragility. Mathematics and Financial Economics, doi: 10.1007/s11579-012-0071-8

Shorto, R. (2012, February 13). The way greeks live now.New York Times. Retrieved from http://www.nytimes.com/2012/02/19/magazine/the-way-greeks-live-now.html?_r=2&exprod=myyahoo&pagewanted=all

Alvaredo, Facundo, Anthony B. Atkinson, Thomas Piketty and Emmanuel Saez, The World Top Incomes Database, http://g-mond.parisschoolofeconomics.eu/topincomes, 10/09/2012.

Andrew Glyn, Capitalism Unleashed, esp. Chs 1-2. Retrieved from http://courses.umass.edu/econ797a-rpollin/Glyn_Chapters%201%20and%202.pdf

The stagnation of the labor market in particular is a grave concern not only because of the enormous suffering and waste of human talent it entails, but also because persistently high levels of unemployment will wreak structural damage on our economy that could last for many years. (Ben Bernanke's Jackson Hole speech)

It is election time in America. For the lawmakers in Washington D.C., the capital of imperium, the emptiness of rousing rhetoric drowning the discomforting discord of American decline is in high season.

But the American situation is not isolated; in a slowing world it is but merely a metaphor for what ails many nations: labour market stagnation begetting increasingly greater inequality as financial capital is judge and jury over putatively sovereign domestic fiscal policy. Growth of the sustainable variety built upon a foundation of a rising standard of living and wage growth can be a cure during normal times but it is merely a palliative for these times where growth requires the catalyst of endless easy credit: these times are anything but normal; there are greater forces at work then a mere slowdown of the business cycle.

Former Labor Secretary during the Clinton Administration, Robert Reich, framed it cleverly in an opinion piece for FT.com in dissecting the gaping policy holes of both incumbent and challenger after the Republican and Democratic conventions:

But another explanation for why neither candidate has come up with a concrete plan is profound disagreement even among experts about what’s gone wrong, and a paucity of credible ideas for righting it. Keynesians want more government spending but can’t come up with a convincing scenario for what happens after the pump is primed. The big stimulus in 2009 and 2010 had a positive impact but hardly enough to rescue the economy. Some Keynesians call for more spending, but how much more before credit markets begin to scream? Some want the Fed to keep interest rates near zero, but it’s kept them near zero for almost three years – along with two rounds of “quantitative easing” – with little to show for it.So-called supply-siders want lower taxes and fewer regulations but can’t come up with a convincing argument for why American businesses would hire more workers under those circumstances. After all, much of their current profitability has come from cutting payrolls — either by substituting computers and software or outsourcing the jobs abroad. Why would they hire additional workers, especially when American consumers – whose spending is 70 per cent of the nation’s economic activity – are holding back? Deficit hawks, meanwhile, want to raise taxes and reduce public spending but have no idea how to do this without bringing on another recession as long as private spending remains in the doldrums. And if the economy contracts, the government debt only worsens in proportion. Markets are already spooked by next January’s “fiscal cliff”.

There is no conventional way out of the current morass: the anodyne prescriptions of the past --from both sides of the political spectrum-- do not provide a convincing prelude to realizing making the "trend" growth of the past generation the same for the future.

Monetary stimulus --the great hope that underpins our debates from "is QE3 coming" to "will the ECB set a negative deposit rate" has proven ineffective at the zero bound as analysts have been attempting to explain, since 2008, that better times are around the corner thanks to increasing "confidence" and rising "expectations".

Fiscal stimulus along the lines of similia similibus curanter ("that which can cause can cure") has less potency due to the open nature of advanced economies and the globalization and technological changes (and by extension inequality of opportunity) that underpins it. Freer markets can indeed create efficiency for many (but certainly not all) goods but it is the openness in factors of production abetted by trade agreements that drives down the size of the fiscal multiplier and drives up the amount of fiscal stimulus required to make a substantive difference; under the current arrangement the power of capital easily trumps labour and diminishing labour power since the 1970s has foreshadowed the inequality of today.

On the one hand, traditional stimulus --both fiscal and monetary-- is tellingly ineffective but on the other hand, fast tracking austerity guarantees depression and is tantamount to fiscal Seppuku. Traditional economic analyses are beholden to 'equilibrium' and, as such, we are -- referencing a (wonkish) paper by Matheus Graselli -- in a "bad equilibrium" with a situation of high debt, low employment and low labour share of wages, as described in the original Goodwin model (modified by Australian economic iconoclast, Steve Keen and) extended by Graselli and Costa Lima. (Graselli and Costa Lima, 2012)

How did it come to this? The system that we have know since the decline of the gold standard backing the U.S. dollar gave way to "dollar hegemony" as the greenback remained the reserve currency -- something that the Greek economist, Yanis Varoufakis, has colourfully framed as "The Global Minotaur":

As Varoufakis writes in his recent book, “The Global Minotaur,” the world in which we have been living until recently functioned thanks to the voracious consumption of a different kind of beast. After World War II, the U.S. built up the infrastructure of its European allies as well as its former enemies, all of whom became trading partners. The U.S., with its great industrial and financial might, became the world’s surplus nation: its profits flowed out to its allies in the form of aid and investments. By the early 1970s, however, other countries had robust economies, and the U.S. was a debtor nation. “At that moment, certain very bright men within the American financial hierarchy made a stunning realization,” Varoufakis told me. The realization was that it didn’t matter if the U.S. was the biggest surplus or biggest debtor nation. What mattered was controlling the world’s primary currency, which would allow the United States to continue to recycle the global economic surplus. The idea was not unlike the thinking behind a casino — whichever gamblers are winning or losing, the house, which sets the terms and takes its cut, always wins.

So a new system came into being, in which a huge part of the world’s capital flows went to service debt originating in the United States. American debt, and the need to feed it, would be the modern Minotaur. The Wall Street financial houses became the handmaidens of the Minotaur. “The massive flow of capital into Wall Street gave it the impetus for financialization,” Varoufakis said, referring to the creation of derivatives and other risky financial vehicles. “And so Wall Street created a great deal of private money, with which it flooded the world and created huge bubbles, in the U.S. housing market and elsewhere.” (Shorto, 2012)

"The Global Minotaur" system is sick and suffered a mortal wound in 2008: it is now acting as a cornered animal wounded to the point of rabidity where financialization now consumes in a parasitic rather than facilitates in a symbiotic fashion, and where speculation trumps productivity in the macroeconomy. Anyone who works in the world of high finance will openly admit that there is no lack of capital --those at the top of the pyramid have fantastic amounts of "surplus capital": portfolio flows globally looking for the highest return and it does so at the push of a keystroke depending on whether the markets are risk averse or risk neutral and across a range of asset classes. The unintended outcome is that laissez faire has led to the accumulation of wealth into fewer and fewer hands and, as outlined in a previous post, Wealth does not trickle down.

But why should we care about the results of a wounded Global Minotaur? Unlike Theseus leading the Athenians out of the labyrinth, the majority of people have nothing but blind folded politicians to guide them from the maze that is the global economy. We need to re-frame the argument into a long term solution that is sustainable but doing so requires looking at some uncomfortable truths: be it rising inequality, growth of non-productive sectors, or the anemic labour market.

Inequality matters

It always has; it is just that we have been too predisposed to notice its importance when it occurs and believe we are immune until it hits us.

This is not advocacy for equality of outcomes: people have different levels of drive, different talents, different motivations. (We are never going to embrace a utopia where we may be idle and spend our leisure time reading poetry and philosophizing).

This is not advocacy for equality of outcomes: people have different levels of drive, different talents, different motivations. (We are never going to embrace a utopia where we may be idle and spend our leisure time reading poetry and philosophizing).

Everywhere, there are those who are indolent, but equally those who are industrious.

What nations require is a greater chance of upward mobility for all of their citizens not an increasing likelihood of indigence due to greater structural unemployment thanks to a policy framework that disregards politics and relies on abstractions based on political motivations.

This is advocacy for greater equality of access: to education, public services, healthcare, and opportunity. Without such building blocks the foundation of society withers and no amount of a Burkean "Big Society", as advocated by its adherents, will take its place.

What nations require is a greater chance of upward mobility for all of their citizens not an increasing likelihood of indigence due to greater structural unemployment thanks to a policy framework that disregards politics and relies on abstractions based on political motivations.

This is advocacy for greater equality of access: to education, public services, healthcare, and opportunity. Without such building blocks the foundation of society withers and no amount of a Burkean "Big Society", as advocated by its adherents, will take its place.

The case against "excessive" equality

The case against inequalityAn excessively equal income distribution can be bad for economic efficiency. Take, for example, the experience of socialist countries, where deliberately low inequality (with no private profits and minimal differences in wages and salaries) deprived people of the incentives needed for their active participation in economic activities—for diligent work and vigorous entrepreneurship. Among the consequences of socialist equalization of incomes were poor discipline and low initiative among workers, poor quality and limited selection of goods and services, slow technical progress, and eventually, slower economic growth leading to more poverty. (Source: World Bank: Beyond Economic Growth An Introduction to Sustainable Development (Chapter V: Income Inequality))

It may seem counterintuitive that inequality is strongly associated with less sustained growth. But too much inequality might be destructive to growth. Beyond the risk that inequality may amplify the potential for financial crisis, it may also bring political instability, which can discourage investment. Inequality may make it harder for governments to make difficult but necessary choices in the face of shocks, such as raising taxes or cutting public spending to avoid a debt crisis. Or inequality may reflect poor people’s lack of access to financial services, which gives them fewer opportunities to invest in education and entrepreneurial activity. (Berg and Ostry, 2011)

(Berg and Ostry, 2011: p. 14)

How is equality measured?

Source: http://visualeconomics.creditloan.com/income-distribution-by-country/

Trends of income shares to the top 1% (1970 - 2009/2010)

The charts below show the income shares (in Australia, Canada, United Kingdom and United States) accruing to the top 1% from the 1970s on and the data was made available by Atkinson, Piketty and Saez of the Paris School of Economics. Go to their website to see these and many more data sets highlighting how inequality is at the highest rate since the 1920s.

Source: The World Top Incomes Database

Canadian Wage Distribution Dynamics

The following charts are from a presentation by Paul Jacobson, "Recent Wage Dynamics - Working Paper" that shows inequality in the Canadian context.

Social and Economic Mobility

The following charts are from a presentation by Miles Corak, "Social and Economic Mobility in Canada"

A Broken Economy: What it isn't

A stylized representation of flows in an economy is often represented by something akin to the diagram below, however, reality checks have been inserted to remind us that money matters, as does class (more on that below). Since money matters, by implication so does the debt, and advanced economy households are in a debt overhang.

It should be noted that Gennarro Zezza, a student of the late Wynne Godley --whose stock-flow consistent modeling provided an red flag to global imbalances in the early 2000s-- stated that:

in the economy – and therefore in models representing the economy - everything comes from somewhere and goes somewhere else: 'there are no black holes.' This obvious principle has relevant implications: one is that the debt of somebody is a credit for somebody else.

But simply because the debt of somebody is a credit for somebody else does not mean that it is not a problem. The financialization of modern economies requires incorporation of rentier sectors into a financial model since much credit has been granted for speculative rather than productive activities in the so-called FIRE (finance, insurance, real estate) sector:

This view is in stark counterpoint to conventional analysis by establishment shills (link courtesy of Charles Ferguson's "Inside Job"):Debt-leveraged buyouts and commercial real estate purchases turn business cash flow (ebitda: earnings before interest, taxes, depreciation and amortization) into interest payments. Likewise, bank or bondholder financing of public debt (especially in the Eurozone, which lacks a central bank to monetize such debt) has turned a rising share of tax revenue into interest payments. As creditors recycle their receipts of interest and amortization (and capital gains) into new lending to buyers of real estate, stocks and bonds, a rising share of employee income, real estate rent, business revenue and even government tax revenue is diverted to pay debt service. By leaving less to spend on goods and services, the effect is to reduce new investment and employment. (Hudson and Bezemer, 2012)

For instance, Mishkin (2012: pp. 1 and 24) explains that “in our economy, nonbank finance also plays an important role in channeling funds from lender-savers to borrower-spenders…

Finance companies raise funds by issuing commercial paper and stocks and bonds and use the proceeds to make loans that are particularly suited to consumer and business needs”. (Hudson and Bezemer, 2012)

A Broken Economy: What it is

Overall model of the FIRE (Finance, Insurance, Real Estate) sector: producers, consumers, government, world (Hudson and Bezemer, 2012: Fig. 4, p.9) based on the U.S. economy primarily but just as relevant to other nations such as the United Kingdom, Spain and Ireland who have suffered real estate asset crashes.

Class Matters

Only a portion of FIRE sector cash flow is spent on goods and services. The great bulk is recycled into the purchase of financial securities and other assets, or lent out as yet more interest-bearing debt – on easier and easier credit terms as the repertory of bankable direct investments is exhausted. So the pressing task today is to trace how directing most credit into the asset markets affects asset prices much more than commodity prices. Loan standards deteriorate as debt/equity ratios increase and creditors ‘race to the bottom’ to find borrowers in markets further distanced from the ‘real’ economy. This increasingly unproductive character ofcredit explains why wealth is being concentrated in the hands of the population’s wealthiest 10 percent. It is the dysfunctional result of economic parasitism. (Hudson and Bezemer, 2012: pp. 10-11)

While Arthur Laffer and Stephen Moore continue to use their pulpit at the Wall Street Journal to conclude that the issue of class should be a non issue as "wealth trickles down" in their worldview, the facts on the ground are quite different. The current situation of inequality was built after the embers of the defunct "Golden Age of Capitalism" burnt out conclusively in the 1970s.

At the end of the 1970s, capital rose to prominence and put an end of the power of labour. The concept of wage growth being tied to productivity has been tenuous since then and has been severed for those down the value chain as there are structural mismatches to the skills people have to the jobs available due since many of the jobs are unlikely to return. As I have outlined previously in 2011 the conventional view, articulated by Raghuram Rajan, is that increased inequality has been the by product of technology and globalization. If we add to the mix the tripling of the global labour pool (or "reserve army of labour" in the Marxian sense) and the fact that a greater share of corporate profits go to those at the top -- despite no substantive proof that the CEOs have become more productive than their counterparts a generation back when compared to the people below -- we have the ingredients for more inequality in society and by extension greater instability in economic growth. This was successfully papered over for a generation by virtue of the credit spigot opening and access to credit increasing but exponential growth in credit reached a tipping point in 2008. But now, we see the reality of people living within their means, paying down debt, and unable to plan for the future due to a lack of job security. The traditional life-cycle hypothesis becomes less realistic in this case:

What happens when that salaried professional referenced above "whose life prospects are reasonably certain and whose life experience reinforces the notion that he or she is "in control" gives way to a growing cohort of people whose jobs have been outsourced, who work on a contract basis, who lack security and whose career prospects are uncertain at best? We have, in the words of Professor Guy Standing, a group of people living precariously: we have the precariat.

The global precariat is not yet a class in the Marxian sense, being internally divided and only united in fears and insecurities. But it is a class in the making, approaching a consciousness of common vulnerability. It consists not just of everybody in insecure jobs – though many are temps, part-timers, in call centres or in outsourced arrangements. The precariat consists of those who feel their lives and identities are made up of disjointed bits, in which they cannot construct a desirable narrative or build a career, combining forms of work and labour, play and leisure in a sustainable way.

Because of flexible labour markets, the precariat cannot draw on a social memory, a feeling of belonging to a community of pride, status, ethics and solidarity. Everything is fleeting. They realise that in their dealings with others there is no shadow of the future hanging over them, since they are unlikely to be dealing with those people tomorrow. The precariatised mind is one without anchors, flitting from subject to subject, in the extreme suffering from attention deficit disorder. But it is also nomadic in its dealings with other people.

Although the precariat does not consist simply of victims, since many in it challenge their parents' labouring ethic, its growth has been accelerated by the neoliberalism of globalisation, which put faith in labour market flexibility, the commodification of everything and the restructuring of social protection.(Guy Standing, "Who will be a voice for the emerging precariat?", guardian.co.uk)

The salariat, proficians and old working class are described by Standing below.There was even a famous “yacht war” that got started in 1997 among the super-wealthy, competing with each other for the biggest. First, Leslie Wexner of Limited Brands bought a 316-foot vessel, some 110 feet longer than anything in its category. That cost about $300 million. But Russia’s Roman Abramovich outdid him, buying three super-yachts of the same kind. Then Paul Allen, cofounder of Microsoft, outdid them both, with a 413-foot yacht that boasts a basketball court, a heliport, a movie theater, and a submarine in the hold. (Jerry Mander, Rule by the Rich, New Left Project)

And for those who believe that higher education is a way out of precarious living, think again for it is the academic precariat that makes up the bulk of higher learning within the North American system of tertiary education: (See video: "Now That I'm Relevant, I Can't Get a Job")

In terms of income, the group below the elite and other representatives of capital is the ‘salariat’, those with above average incomes, with an array of enterprise benefits and employment security. This group is shrinking, hit by the financial crisis, austerity packages and the extension of labour market flexibility, nowhere more so than in Greece.

Some of the salariat have joined the third group, ‘proficians’, those with bundles of technical and emotional skills that allow them to be self-selling entrepreneurs, living opportunistically on their wits and contacts. This group is growing but is relatively small; it tends to be socially liberal but economically conservative, since it wants low taxes and few obstacles to money making.

Below the salariat and proficians in terms of income is the old manual working class, the proletariat, which has been dissolving for decades. The democracy built in the twentieth century was designed to suit this class, as was the welfare state. Trades unions forged a labourist agenda and social democratic parties implemented it. That agenda has little legitimacy in the twenty-first century. (Guy Standing, The Precariat: why it needs deliberative democracy, 27 January 2012, opendemocracy.net)

(Source: USCRossier - Pullias Center for Higher Education, The Changing Faculty and Student Success)

To be certain, some of those who share the political spectrum with Guy Standing have a big problem with his class analysis and quip over the need to meddle with the old fashioned Marxian (bourgeois vs. proletariat) dichotomy but this does not change the data: more people live precarious lives, societies are experiencing greater inequality, household sectors in major economies are recovering from a debt overhang while governments struggle with fiscal initiatives as they worry about what will be acceptable to credit markets and central banks prove the impotence of monetary policy (at the zero lower bound) with each passing meeting as we struggle to resuscitate a dying economic system.

I have gone on record about my views about the future in previous posts; will policy makers continue to use the tools of the past to fight the problems of today or will revolutionary thinking come to the fore? They have failed to rise to the occasion except for saving the banks. But saving the banks has not saved the world; some of the banks have become zombies whilst the remainder are looking for opportunities to deploy risk capital in a world of spread compression.

Demographic headwinds (in the Canadian context summarized here but a challenge everywhere) will only add to the puzzle. The U.S. Federal Reserve's zero interest rate and quantitative easing policies will effectively kill many defined benefit plans in the America and thus create a larger precariat over there with their diminished pension benefits.

What we need is less inequality and greater equality in access to opportunity. Looking for global trade access to the emerging world is not a panacea but a small part of the solution as the BRICS nations (amongst others) have problems of their own to deal with.

The problems remain but are the solutions forthcoming?

To begin, citizens need to be re-connected with the democratic process; if people spent a fraction of their time that they devote to distractions (such as what is on reality television or how will the NHLPA and NHL owners divide the billions in revenue) on political engagement then politicians will take note rather than assume that we are a disengaged citizenry willing to eat rhetorical pablum.

To begin, citizens need to be re-connected with the democratic process; if people spent a fraction of their time that they devote to distractions (such as what is on reality television or how will the NHLPA and NHL owners divide the billions in revenue) on political engagement then politicians will take note rather than assume that we are a disengaged citizenry willing to eat rhetorical pablum.

The opinions reflected in the post 'Growth falters, and inequality grows as capital flows' are those of the author. Any errors and omissions are the author's alone.

Notes:

Labour vs. labor: I have attempted to stick to the Canadian/British spelling of labour in the neutral context but when referring specifically to the United States, the American spelling has been used.References:

Bernanke, B. (08, 2012 31). Monetary policy since the onset of the crisis. Retrieved from http://www.federalreserve.gov/newsevents/speech/bernanke20120831a.htm

Hudson, M., and Bezemer, D. (2012). Incorporating the rentier sectors into a financial model. World Economic Review, 1(1), 1-12. Retrieved from http://wer.worldeconomicsassociation.org/article/view/36

Reich, R. (2012, September 07). After the politics, the reality of the us labour market. Financial Times. Retrieved from http://blogs.ft.com/the-a-list/2012/09/07/after-the-politics-the-reality-of-the-us-labour-market/

Berg, A. G., & Ostry, J. D. (2011).

Equality and efficiency.FINANCE and DEVELOPMENT, 48(3), 12-15. Retrieved from http://www.imf.org/external/pubs/ft/fandd/2011/09/Berg.htm

Graselli, M. R., & Costa Lima, B. (2012). An analysis of the Keen model for credit expansion, asset price bubbles and financial fragility. Mathematics and Financial Economics, doi: 10.1007/s11579-012-0071-8

Shorto, R. (2012, February 13). The way greeks live now.New York Times. Retrieved from http://www.nytimes.com/2012/02/19/magazine/the-way-greeks-live-now.html?_r=2&exprod=myyahoo&pagewanted=all

Alvaredo, Facundo, Anthony B. Atkinson, Thomas Piketty and Emmanuel Saez, The World Top Incomes Database, http://g-mond.parisschoolofeconomics.eu/topincomes, 10/09/2012.

Andrew Glyn, Capitalism Unleashed, esp. Chs 1-2. Retrieved from http://courses.umass.edu/econ797a-rpollin/Glyn_Chapters%201%20and%202.pdf

No comments:

Post a Comment